7 simple steps to grow your fortune!

Here’s something that may be of use to you!

Who doesn’t want to have more money? Most everyone it seems! Just look at their spending and borrowing habits. Clearly these people want to be poor. They think poor. They act poor. Their comfortable being poor. They’ve made the decision to value their lifestyle over and above their financial and personal well being. And who can blame them? Saving and growing money is hard.

That’s right, I just told you that adding to your personal fortune is HARD! That’s the truth. Too many people are out there giving others positive reinforcement and pats on the back for making bad financial decisions. I’m not going to do that here. I want to tell you the truth.

Obviously the following 7 tips are not universal, but most people will be able to leverage at least a few of them in their day to day life. If you do follow them I can promise you that you will cut the amount of money flowing out of your personal empire and be able to build a better and more secure life. These tips are hard, but they are also simple.

1. Cut the Starbucks.

Starbucks started in 1971 and, within just a couple of decades, grew to become an international phenomenon. That’s great! Good for them. Bad for you.

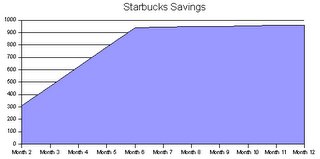

In order for them to plant their nearly 6000 stores they had to addict you to a $5 a day cup of overpriced caffeine. Some may call it evil, others might call it good marketing, but the reality is that it kills your ability to save and invest money. How much damage does it do?

Lets suppose that you were able to save the $5 you spend a day on Starbucks or some equivalent product and invest it in a savings account with a conservative return of %4. Lets say you just do this for the first six months of the year and then go back to your normal habit after that. How much money would you have in your account at the end of the year?

Over $950! That’s right. In just a year, with 6 months of sacrifice, you’d have close to $1000 and have earned about $30 in interest. Neat, huh? Think of what giving it all together could do!

2. Follow the 5% rule.

I’m going to assume you have some personal debt (most people do you know). Maybe some student loans, couple of credit cards, mortgage, 2nd mortgage, 3rd mortgage, car loan, yatch loan…you get the idea. The 5% rule says you should put into savings 5% of the funds you use to pay your recurring loan payments. How’s that? Well lets say you pay $700 a month on loans (including money going to principle), following the 5% rule you would need to put $35 into savings. Why? Because not having money in savings is why you took out loans in the first place! Don’t want that to happen again, do we?

Notice that over 10 years that $35 a month could turn into over $5000 in savings.

3. Don’t be fooled by “deals.”A while back I nearly signed up for a preferred membership with Barns and Noble. It offered me 10% off all my book buys and only cost $25 a year. Only costs $25 a year! What am I, an idiot? I’d have to buy $250 worth of books to even cover the cost. If I really plan on buying that many books in a year I should darn will prepare ahead of time and buy them online, getting free shipping and up to 35% of the cover price at places like Buy.com and Amazon.com.

Remember the golden rule that companies follow when they offer you a deal: do unto your customers that which makes you more money. Don’t buy memberships. Don’t buy stuff simply because its “on sale.” Don’t buy anything off of TV. And, more importantly, don’t buy anything unnecessary at the time its being sold to you. If you need it now you’ll need it in two weeks. If you don’t need it in two weeks (or don’t remember to go back and buy it) you’ve just saved yourself some money.

4. Use Credit Cards as a form of Payment, not Credit.

Last year I got a DiscoverCard and used it throughout the year on every-month purchases such as gas, food, and various types of entertainment. I faithfully paid the full amount each time I got a bill, and do you know what happened? By Christmas I’d earned enough of a dividend (1% on all purchases, 5% on certain types of purchases) to pay for nearly all the presents I purchased.

You don’t have to go with Discover. Chase offers a rewards Visa and Citi offers a rewards Mastercard.

Remember, the worst thing you can possibly do for yourself is to dip your hand in super heated melted plastic. Especially if it’s pink. Ugh! The second worst thing you can do is carry a balance on your credit cards!

5. Open a high yield online savings account.

My bank pays me just less than 1% interest on my savings account. Nice of them huh? This is up considerably from a few years ago when finding money in parking lots brought in a lot more income than savings accounts. Now days there are a number of competitive online savings accounts (still FDIC insured) that offer rates as high as 4.25%. If you don’t have one of these accounts you should get one. ING offers a good one at 4.75% (for a limited time, 3.8% normally). Emigrant Direct as one that pays 4.25%. And HSBC has one paying 4.25% with $25 sign up bonus (use promo code: start) and an ATM card. All are free and simple to use with your existing checking account.

6. Save before you pay your bills.

I don’t care how much money you save, just start saving. Make saving the first thing you do after pay day. The more money “out of your hands,” the better. If you don’t have an extra $20 to spend on movie night, so much the better! Try going for a walk or watching the sunset instead. Hollywood won’t be the worse for wear and you’ll be in better financial shape for it. Do whatever you can to not tempt yourself to spend money when you don’t need to. And “need to” is defined as pre-ordained in the budget.

7. Choose a less consumer-centric lifestyle.

You know you’ve done it. You know you’ve laughed at a friend when they got all caught up in the latest reality TV show, clothing style, music artist, or “Warcrack” video game. But did you stop to think that you get played by the same big money cycle of consumerism everyday? Why not stop? Then you can laugh at all your friends as they mindlessly return to Walmart again and again. Ho! Ho!

Ok, so laughing may be kind of cruel. How about leading them? Listen when I tell you that the George Foreman Grill, the subscription to Esquire, the flat screen TV, the Herbal Essences Shampoo, the entire collection of McDonald’s Beanie Babies, and the latest and greatest in trash bag technology is never going to make you happy or attractive. Look at the people you know who have them. Are they happy? Or do they just want more stuff?

Ask yourself one question right now, do you want an IPOD with 5000 of your favorite (legal!) music tracks or would you rather be able to pay for treatment to help a loved one suffering from severe back pain? Well I can tell you this much, you’re not going to get closer to either goal with that pack of Bubblicious gum in your hand. So put it back on the shelf, pay for the stuff you need, and run! Run for your life. Run for your health. Run for your happiness. And run for your fortune!

Source: Credit Review Blog

1 thought on “7 simple steps to grow your fortune!”

Cees April 13, 2007 at 5:32 am

Cees…

I do think you right on the spot with this post, i could use a lot a struff for my new study thank you very much.

Greets …